Economic & Housing Update May 5, 2023

Economic & Housing Update May 5, 2023

The Fed signals that it may be done hiking rates this year as the labor market remains hot

Summary:

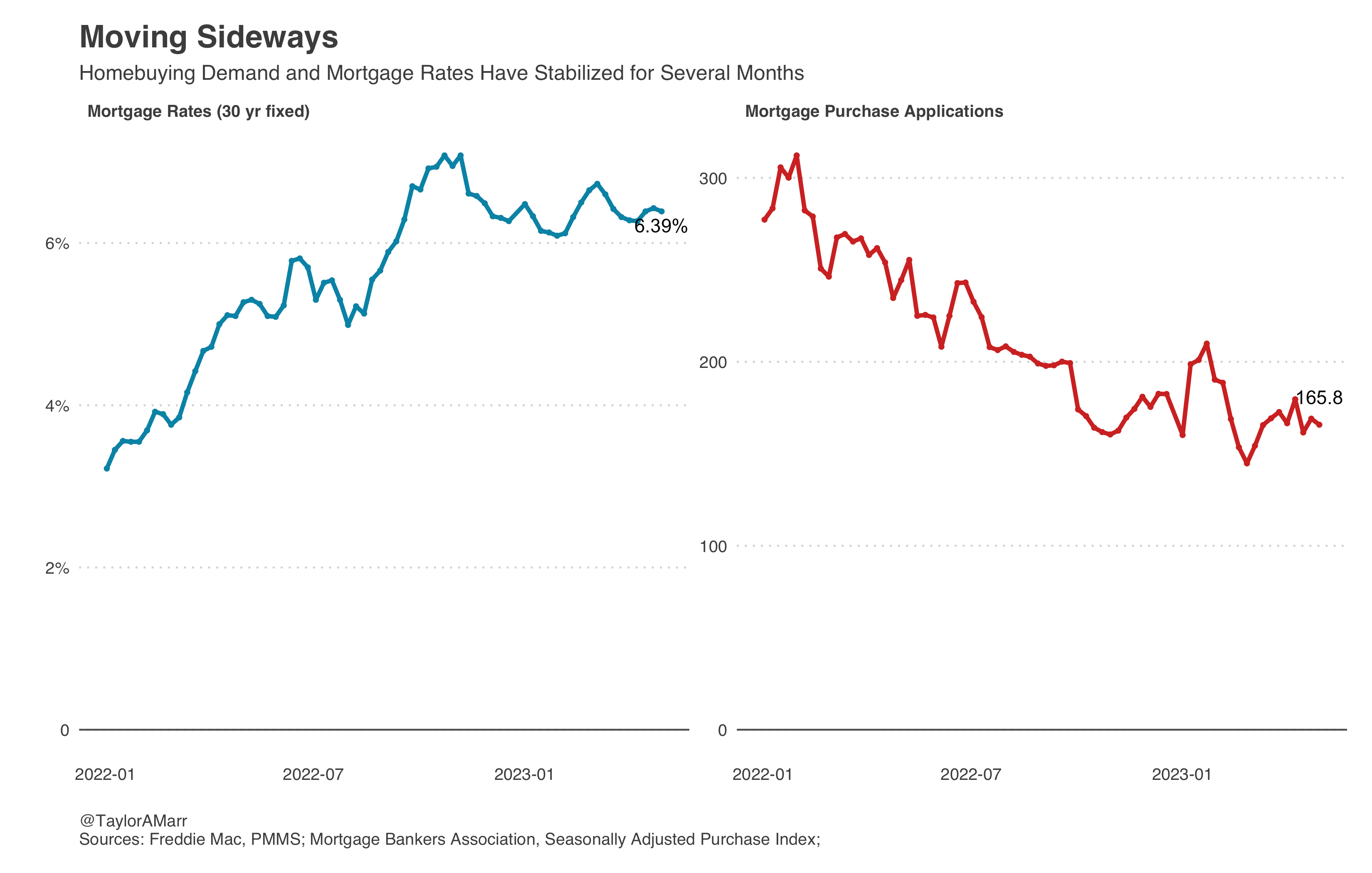

Mortgage rates fell slightly this week to 6.39%, but have mostly moved sideways for six months. There was little new data for the housing market this week.

The Federal Reserve raised the fed funds rate by 25bps to a range of 5%-5.25% and signaled that it may be done with a tightening cycle. Futures markets point to no further rate hikes ahead.

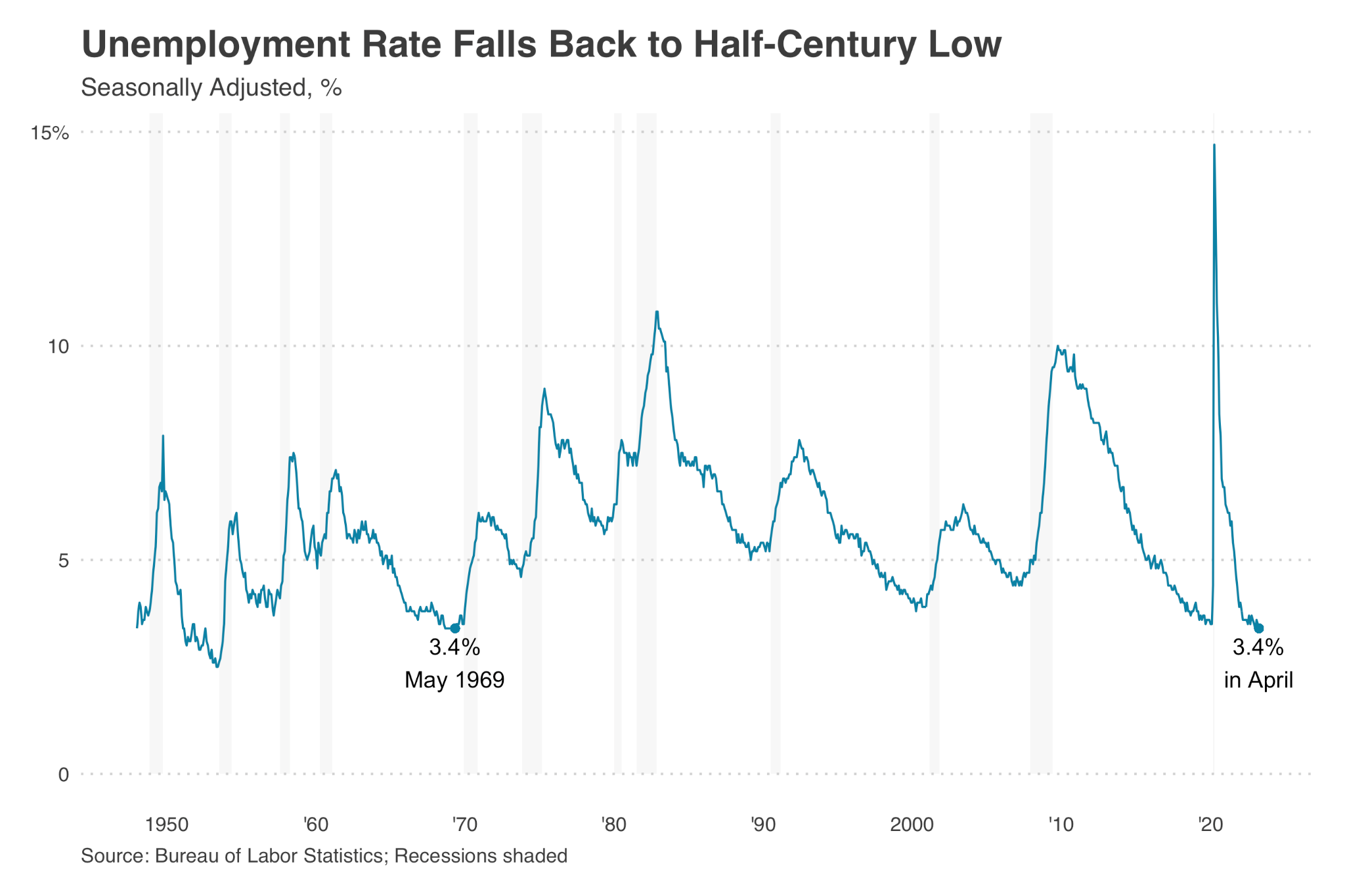

Job openings in March dropped by more than expected as layoffs also ticked up in March. However, most of those workers appear to be finding jobs given that the unemployment rate unexpectedly fell to 3.4% in April as the US economy added 253K jobs and wage growth reaccelerated.

This week had as many ups and downs as any. Fundamentally, we learned that the US economy is doing alright still and far from a recession still. Data from the Institute for Supply Management (ISM) revealed better than expected improvements in manufacturing and services in April. The US trade gap also narrowed to a four-month low amidst rising exports and a slight decline in imports. As a result, the latest nowcast for Q2 GDP rose to 2.7% from 1.8% a week earlier. On Wednesday, Fed Chair Powell reiterated that he is still expecting a soft-landing for the economy this year and that appears slightly more likely, given the data this week. The Fed hiked rates above 5% to the highest level since 2007, but also signaled that they may be done with further rate hikes in changes to their policy statement.

In order to achieve a soft-landing the labor market needs to cool further, but also not break. This week we received mixed signals at first glance. On the cooling front, job openings fell faster than expected in March, while layoffs increased. Throughout April, jobless claims continued to rise. But, it appears that many laid-off workers have been able to find work in other companies and industries, since the unemployment rate for April fell to 3.4%—a half-century low—compared to an expected increase to 3.6% (see chart). Job gains were also greater than expected at 253,000 new jobs and monthly wage growth jumped to 0.5% from 0.3%. That said, the data is even more complicated as the previous month’s job gains revised down, leading us to conclude that the labor market is still cooling down, but not breaking.

So what does all this mean for housing? Mortgage rates didn’t change much this week in the end, according to Freddie Mac (see chart). Most of the housing data is moving sideways—not worsening, but not improving much either. For now, home sales are still very constrained by the lack of new supply hitting the market, which is still down 23% from a year earlier. Until rates can move closer to 6% or lower, the housing market will continue to feel strange—fast and competitive, yet less active at the same time.

New housing data:

The homeownership rate in the U.S. ticked up to 66% in the first quarter of 2023, according to the Census Bureau. National vacancy rates in the first quarter were 6.4 percent for rental housing and 0.8 percent for homeowner housing. The rental vacancy rate was higher than the rate in the first quarter of 2022 (5.8 percent) and higher than the rate in the fourth quarter of 2022 (5.8 percent).

The MBA Purchase Index decreased 2% to 165.80 points in the week ended April 28th 2023. The adjustable-rate mortgage (ARM) share of activity increased to 7.3 percent of total applications. “The jumbo-conforming spread continues to narrow, an indication that there is reduced lender appetite for jumbo loans following the recent turmoil in the banking sector and heightened concerns about liquidity. The spread was 13 basis points last week, after being as wide as 64 basis points in November 2022.”

This week, mortgage rates inched down slightly to 6.39% amid recent volatility in the banking sector and commentary from the Federal Reserve on its policy outlook, according to Freddie Mac. Daily rates from MND decreased to 6.5% from 6.73% at the start of the week.

March brought a seasonal increase in home showing traffic, according to the latest data from the ShowingTime Showing Index®. Tours were down 21% in March, but the overall index was still 33% and 43% higher than in 2018 and 2019, respectively. The overall increase in showing activity was driven by the Midwest, up 18% from February, and the Northeast, up 15%. The South stayed relatively flat with a monthly increase of 1.4%, and the West dropped 2.7%, reversing its trend of steady monthly showing growth since late last year.

Redfin’s weekly report revealed that “the total number of homes for sale has steadily declined over the last month, going against the typical spring inventory bump. Pending home sales were down 16.8% year over year. They rose 3% on a month-over-month basis—typical for this time of year. New listings of homes for sale fell 22.9% year over year, the second-biggest decline since May 2020.”

New economic data (source):

The ISM Manufacturing PMI in the United States rose to 47.1 in April 2023, up from a three-year low of 46.3 in the previous month and slightly above market consensus of 46.8. Still, the latest reading suggested economic activity in the manufacturing sector shrank for a sixth consecutive month, as higher borrowing costs and tight credit hit activity and boosted the risk of a recession this year.

The ISM Services PMI increased to 51.9 in April of 2023 from 51.2 in March, and slightly higher than market expectations of 51.8. It marks a fourth consecutive month of growth in the services sector. On the other hand, production rose at the slowest pace since May 2020 (52 vs 55.4) and employment growth also slowed (50.8 vs 51.3). Meanwhile, price pressures were slightly higher (59.6 vs 59.5) and backlog of orders fell less (49.7 vs 48.5).

The number of job openings dropped by 384,000 to 9.6 million in March 2023, the lowest level since April 2021 and below the market's expectation of 9.775 million, indicating that the labor market may be cooling off. Over the month, job openings decreased in transportation, warehousing, and utilities (-144,000) but increased in educational services (+28,000). Meanwhile, the number of hires and total separations remained relatively stable at 6.1 million and 5.9 million, respectively. Within separations, the number of quits (3.9 million) did not show significant changes, while layoffs and discharges (1.8 million) increased.

The Federal Reserve raised the fed funds rate by 25bps to a range of 5%-5.25% during its May meeting, marking the 10th increase and bringing borrowing costs to their highest level since September 2007. The decision came in line with market expectations. The central bank also signaled that it may be done with a tightening cycle by taking out from the statement sentence pointing to the need for additional policy firming. Still, policymakers added that in determining the extent to which additional policy firming may be appropriate, they will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments. Officials also noted that although the U.S. banking system is sound and resilient, tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation and the extent of these effects remains uncertain.

The US trade gap narrowed to a four-month low of $64.2 billion in March of 2023 from $70.6 billion in February, compared to market forecasts of a $63.3 billion gap. Exports went up 2.1% to $256.2 billion, prompted by sales of crude oil, fuel oil, natural gas, passenger cars and travel. Meanwhile, imports edged 0.3% lower to $320.4 billion. Considering Q1, the goods and services deficit decreased $77.6 billion, or 27.6% from the same period in 2022. Exports increased $61.4 billion or 8.7% and imports decreased $16.2 billion or 1.6%.

The number of Americans filing for unemployment benefits rose by 13 thousand to 242 thousand in the week ending April 29th, surpassing market expectations of 240 thousand. The result compounded recent data that points to a marked softening of the US job market, caving to a prolonged series of aggressive interest rate hikes by the US Federal Reserve. The four-week moving average, which removes week-to-week volatility, rose by 3,500 to 239,250.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2023 is 2.7 percent on May 4, up from 1.8 percent on May 1. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the Institute for Supply Management, the nowcasts of second-quarter real personal consumption expenditures growth and second-quarter real gross private domestic investment growth increased from 1.3 percent and 1.0 percent, respectively, to 2.1 percent and 2.7 percent, while the nowcast of the contribution of the change in real net exports to second-quarter real GDP growth decreased from 0.38 percentage points to 0.31 percentage points.

The US economy unexpectedly added 253K jobs in April 2023, beating forecasts of 180K and following a downwardly revised 165K in March. The April number largely exceeds the 70K-100K monthly job gain needed to keep up with growth in the working-age population and compares with the average monthly gain of 290K over the prior 6 months. The March reading was revised sharply lower to 165K from an initial estimate of 236K. The unemployment rate edged down to 3.4% in April 2023, matching a 50-year low of 3.4 percent seen in January and below market expectations of 3.6 percent. Meanwhile, the labor force participation rate was unchanged at 62.6 percent. Average hourly earnings for all employees on US private nonfarm payrolls rose by 0.5% in April 2023, after a 0.3% increase in the prior month, while analysts had expected them to remain steady at 0.3%. It was the fastest increase in average hourly earnings in nine months.

Have a great weekend,

Taylor Marr