Economic & Housing Update Mar 10, 2023

Economic & Housing Update Mar 10, 2023

Rising layoffs are likely to impact the housing market as mortgage rates remain elevated, despite the SVB debacle pulling down rates today

Summary:

Mortgage rates fell 0.29% over the past two days as the Silicon Valley Bank failure fueled investor concerns, impacting the bond market and overshadowing the highly anticipated jobs report.

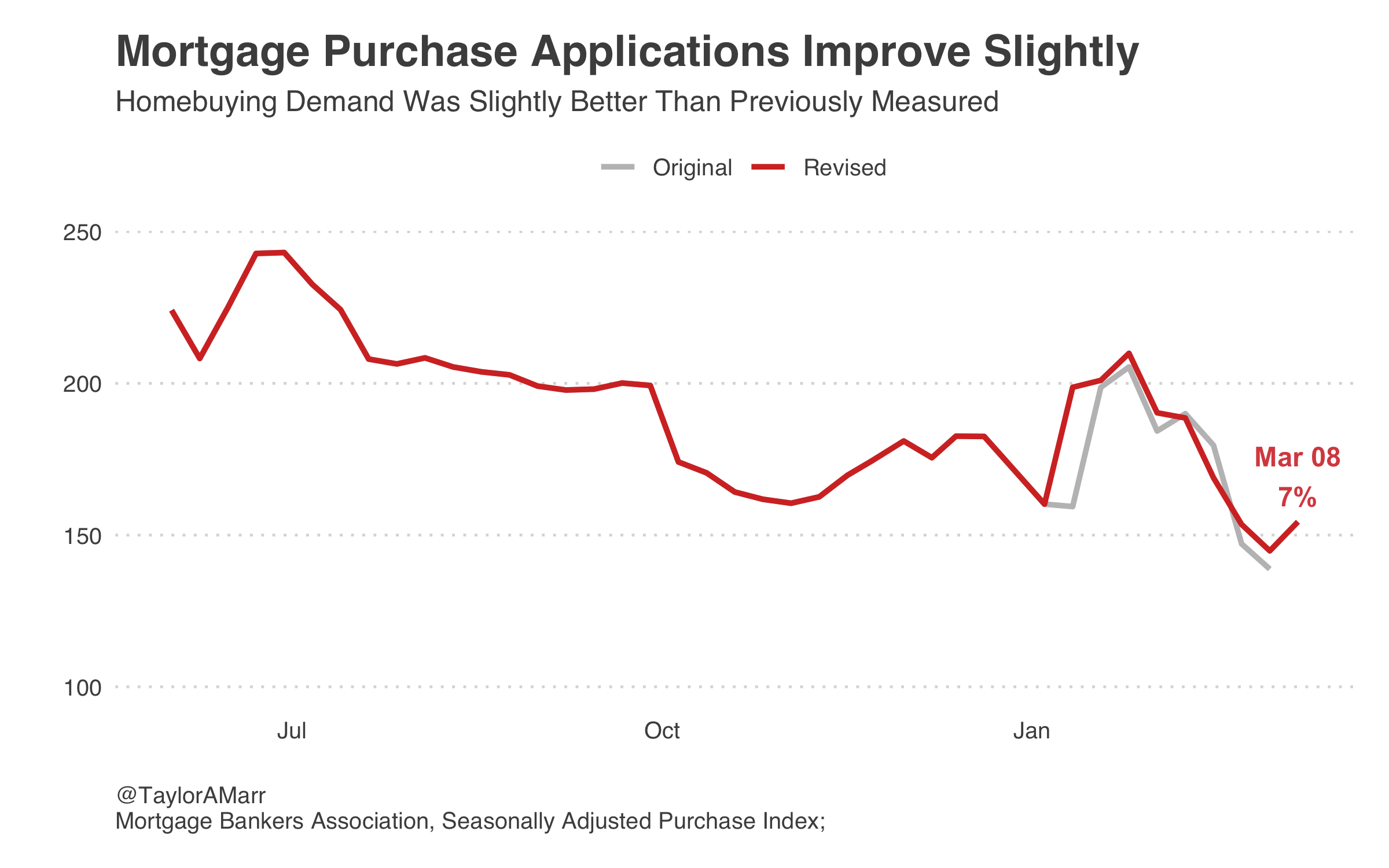

Mortgage purchase applications improve 7% alongside upward revisions for the previous two months. However, other measures of homebuying demand are finally starting to show weakness as touring activity slowed, Redfin’s demand index ticked down 4% and weekly pending sales growth pulled back.

A flurry of labor market reports this week had a key theme—layoffs are rising. The JOLTs data for January showed an increase in layoffs of 241,000 (16%). Today’s Jobs Report for February had an increase in the number of unemployed people by 242,000 (the unemployment rate increased to 3.6% from 3.4%). Finally, jobless claims jumped by 21,000 (10%) to 211,000 for the week ending March 4th.

Today, the collapse of the Silicon Valley Bank (SVB) is the most significant event to impact housing from the week, despite a wealth of anticipated data on the labor market being released. Why? Risk and uncertainty. I won’t get into the specifics of SVB’s failure (read more here), but instead the more important fact is that it is sparking concerns among investors of a potential banking crisis. For now the risks seem contained. The Dodd-Frank Act1 implemented new rules for banks and regulatory oversight that should (in theory) limit the impact of the situation in contrast to 2008. Nonetheless, there is uncertainty that is notable with what happens next and what ripple effects or parallels might unfold. Financial and economic risks are a fundamental driver of long-term bond yields (alongside inflation and economic growth), which is why mortgage rates tanked this week. According to Mortgage News Daily, mortgage rates fell nearly 0.3% since Wednesday. But mortgage rates are still elevated at 6.76%, well above the 5.99% from 6 weeks earlier.

Meanwhile, we learned a lot about the labor market this week from three key reports. They also all had a consistent theme of layoffs being on the rise. First, the Job Openings and Labor Turnover Summary (JOLTS) report for January showed an increase in layoffs of 241,000 (16%) to 1.7 million layoffs (see chart). Job openings fell as well, but the number of openings per worker remains elevated. Yet, the openings are often not in the same sectors as the ones experiencing increases in layoffs. Today’s much anticipated Jobs report for February also had an increase in the number of unemployed people by 242,000; the unemployment rate increased above expectation to 3.6% from 3.4%, but this was also because more people started looking for work, entering the labor force. This was also behind some promising signs of easing wage growth (more workers are easing the pressure on wages), which will help with inflation concerns. Finally, more recent data indicated that jobless claims jumped by 21,000 (10%) to 211,000 for the week ending March 4th.

Collectively, we see that since the start of this year, many people are losing their jobs. Even if these people can find work quickly, this can still have significant impacts in making large decisions like buying or selling a home. Fannie Mae’s Home Purchase Sentiment Index showed that 24% of respondents expressed concern about losing their job in the next 12 months, up from 18% last month. This contributed to an overall reversal in housing sentiment. Most other leading indicators of demand are also showing some weakness and a continuation of layoffs will certainly be a drag on housing demand. According to ShowingTime, showings are falling about 6% behind last year’s increase. Redfin’s demand index ticked down 4% and pending sales growth started to weaken as well headed into March, according to Redfin’s weekly data. These trends are driven by the rise in mortgage rates and follow the abrupt decline in mortgage purchase applications. This week, however, applications increased 7% and data for the past two months also revised up slightly (see chart). If rates go lower, we may see more stability in demand this spring.

New housing data:

The Fannie Mae Home Purchase Sentiment Index® (HPSI) decreased 3.6 points in February to 58.0, breaking a streak of three consecutive monthly increases and returning the index closer to its all-time survey low set in October 2022. Overall, four of the HPSI’s six components decreased month over month, most notably those associated with job security and home-selling conditions. While both components remain positive on net, in February 44% of consumers reported that it’s a bad time to sell a home, up from 39% last month, and 24% expressed concern about losing their job in the next 12 months, up from 18% last month. Year over year, the full index is down 17.3 points.

The MBA Purchase Index increased 6.6% to 154.4 in the week ended March 3rd 2023. The index for previous weeks was also revised upward after some missing responses were incorporated, resulting in a stronger January jump in applications than previously measured. This week’s increase was 11% above the original print for last week. The adjustable-rate mortgage (ARM) share of activity increased to 8.6 percent of total applications.

Mortgage rates continued to increase to 6.73% in Freddie Mac’s latest survey for the fifth week in a row. But the debacle in banking around SVB along with today’s Jobs Report sent the 10 year down quite a bit at the end of the week, providing some mortgage rate relief on Friday of -24 basis points.

Redfin’s weekly data shows that prices continue to slide—down 1.2% over the year. Higher mortgage rates, however, are also pushing up mortgage payments to a new all-time high.

New economic data (source):

Fed Chair told the US Congress the Fed is prepared to increase the pace of rate hikes, if the totality of the data were to indicate that faster tightening is warranted. Powell also noted that the latest economic data have come in stronger than expected, which suggests that the ultimate level of interest rates is likely to be higher than previously anticipated. The Fed continues to anticipate that ongoing increases in the target range for the federal funds rate will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% and that restoring price stability will likely require a restrictive stance of monetary policy for some time. The Fed raised the target range for the fed funds rate by 25bps to 4.5%-4.75% in its February 2023 meeting, dialing back the size of the increase for a second straight meeting but still pushing borrowing costs to the highest since 2007.

The number of job openings fell by 410,000 to 10.824 million in January 2023 from an upwardly revised 11.234 million in December, compared to market expectations of a 10.5 million decrease. Over the month, the largest decrease was in construction (-240,000). Meanwhile, the number of hires and total separations changed little at 6.4 million and 5.9 million, respectively. Within separations, quits decreased to 3.884 million, the lowest level since May 2021, while layoffs and discharges went up to 1.7 million.

The number of Americans filing unemployment benefits jumped by 21,000 (10%) from the previous week to 211,000 on the week ending March 4th, the most since December 2022 and well above market expectations of 195,000. The latest value was the first upside surprise in one month, diverging from a series of labor data that underscored a stubbornly tight job market and hinting that labor conditions could start to soften.

The US economy unexpectedly created 311K jobs in February of 2023, well above market forecasts of 205K, and following a downwardly revised 504K in January. Notable job gains occurred in leisure and hospitality (105K). On the other hand, employment declined in the information industry (-25K). Employment in information has decreased by 54K since November 2022.

The unemployment rate edged up to 3.6 percent in February 2023, up from a 50-year low of 3.4 percent seen in January and above market expectations of 3.4 percent. The number of unemployed people increased by 242 thousand to 5.94 million and employment levels rose by 177 thousand to 160.32 million. The labor force participation rate inched higher to 62.5 percent, the highest since March 2020.

Have a great weekend,

Taylor Marr

In grad school, I read and analyzed all 848 pages of the Dodd–Frank Wall Street Reform and Consumer Protection Act for my thesis work in relation to the behavioral aspects of the housing bubble.

You read all 848 pages of Dodd Frank??? You might be the only one. :)