Economic & Housing Update Jun 16, 2023

Economic & Housing Update Jun 16, 2023

The Fed continued to slow the pace of rate hikes, but core inflation remains a challenge that is leaving mortgage rates elevated and dampening homebuyer demand

Summary:

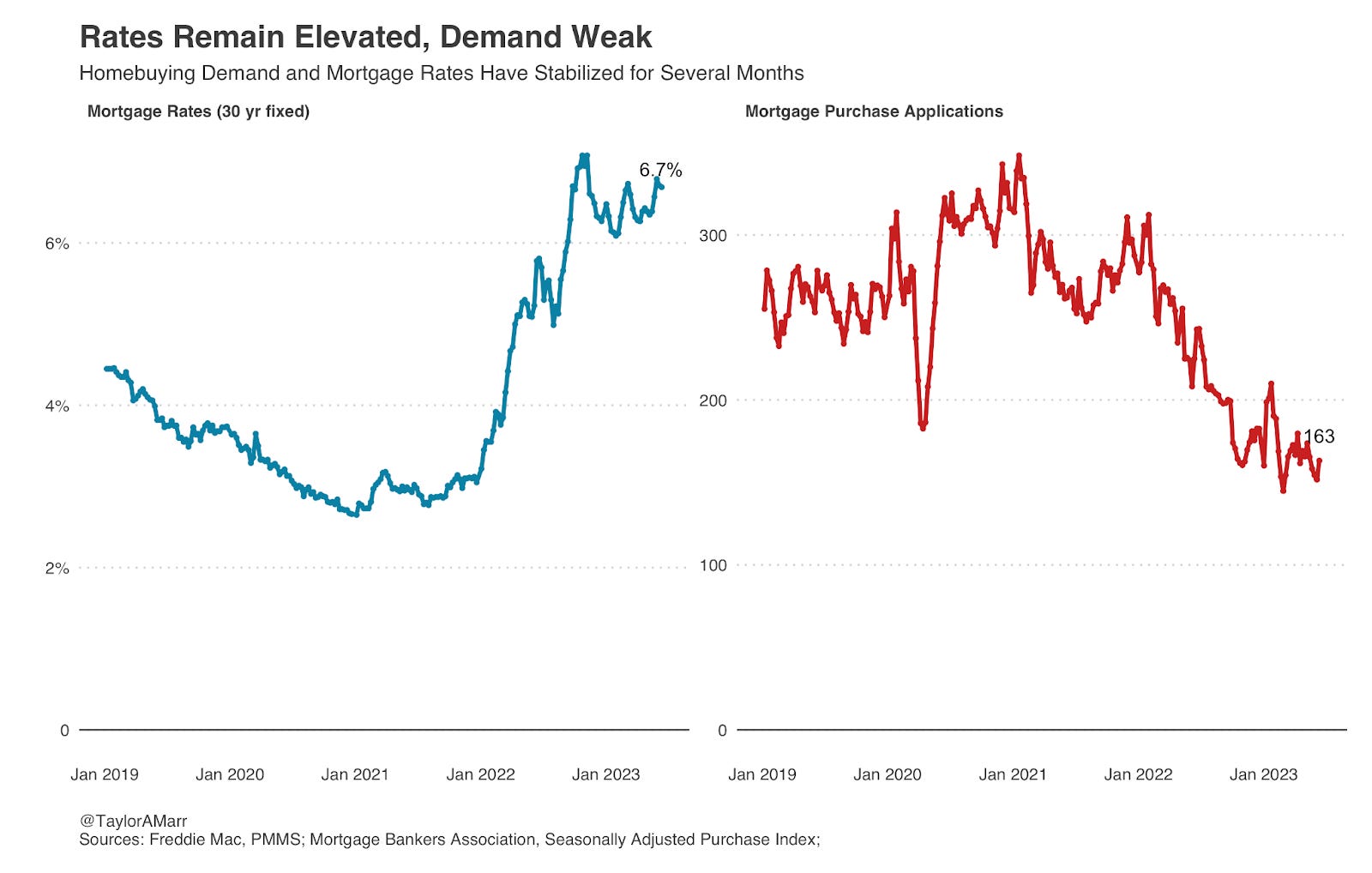

Mortgage rates decreased slightly this week to 6.69%, but remain 30 basis points above four weeks earlier.

Mortgage purchase applications rebounded 7.6% this past week, reversing a month of weekly declines, but is far from recovering.

Home purchase sentiment and mortgage credit availability each ticked down further in May, weighing on the outlook for housing sales. One bright spot was a jump in sentiment for being a “good time to sell” to the highest level since last July.

Headline inflation (CPI) continues to cool in-line with expectations. CPI eased to 4%, while core-inflation remains higher at 5.3%. The Fed held off on hiking the federal funds rate, but signaled 1 to 2 additional hikes by year-end if the economy and inflation do not slow down more.

Greetings after a brief hiatus for a few weeks. While it has been a busy month, it has also been a relatively stable one. Volatility of various forms has declined. The purpose of this newsletter is to highlight at a high level recent developments in the broader economy and tie it back to the housing market. For months, weekly economic developments were surprising and significant enough to shift mortgage rates and the short-term outlook for housing by quite a bit. Now, there is less whip-lash, but still plenty of pain. Core inflation (less food and energy) is above 5%, which is a long way off from where it needs to be. Mortgage rates remain closer to 7% and the federal funds rate range sits above 5% as well. I expected stability to finally arrive at a lower level on each of these metrics. I was wrong. Fed Chair Powell stated on Wednesday that no FOMC participant expects to cut rates in 2023 and market expectations have now shifted higher to reflect that projection (see chart). The Fed now expects 1 to 2 additional rate hikes by the end of the year.

Given the reality that we’re stuck at a place of elevated interest rates and inflation, the housing market will have a difficult time improving much from here in 2023. The housing market not only suffers from high mortgage rates (see chart), which has priced millions of buyers out of the market, but also there is a significant shortage of homes for sale. According to Redfin data, there are nearly 40% fewer homes for sale than pre-pandemic. While this is bolstering prices, it also holds back home sales.

One theory has been that an inevitable drop in inflation and interest rates this year could draw out supply and demand. Unfortunately, it now looks like it will be too late to hit this year’s summer buying season and thus is likely to delay activity to next year. One reason is because most homeowners are rate-locked into sub 5% mortgage rates and it will take a larger drop in rates before they decide to list for sale. That takes time. Barring a wider economic cooldown, the good news is that when inflation does moderate it should help pull down mortgage rates and the loss of activity this year will more likely shift into the next year. Therefore, 2024 may be unexpectedly strong if the Fed can achieve the soft-landing of avoiding a recession and cutting rates.

New housing data:

The Fannie Mae Home Purchase Sentiment Index® (HPSI) decreased in May by 1.2 points to 65.6, as affordability constraints continue to color consumers’ perceptions of homebuying and home-selling conditions. Four of the HPSI’s six components decreased month over month, most notably the component polling consumers’ belief that it’s a “good time to buy,” which is once again nearing its survey low. The “good time to sell” component, however, increased in May to its highest level since last July. The full index is down 2.6 points year over year.

Mortgage credit availability decreased by 3.1 percent to 96.5 in May according to the Mortgage Credit Availability Index (MCAI). A decline in the MCAI indicates that lending standards are tightening, while increases in the index are indicative of loosening credit. The Conventional MCAI decreased 2.3 percent, while the Government MCAI decreased by 3.8 percent. Of the component indices of the Conventional MCAI, the Jumbo MCAI decreased by 1.5 percent, and the Conforming MCAI fell by 3.9 percent.

The MBA Purchase Index in the United States increased 7.6% to 163.20 points in the week ended June 9th 2023.

Mortgage rates decreased slightly this week to 6.69% in anticipation of the pause in rate hikes by the Federal Reserve. As inflation continues to decelerate, economic growth is slowing and the tightening cycle of monetary policy is reaching its apex, which means mortgage rates are expected to decrease later this year and into next.

Freddie Mac published a new outlook that calls for further price declines (3% over the next year) and a weak economic and home sales outlook. The report also reveals that the overall increase in the total homeownership rate can be attributed to the strong growth in the below-median family income homeownership rate, which has sharply increased since 2016 from 48.0% to 53.4%.

New economic data (source):

US consumer inflation expectations for the year ahead fell to 4.1% in May 2023, the lowest since March 2021. The median inflation for the next 12 months is expected to moderate further for rent (down by 0.1 pp to 9.1%). Meanwhile, inflation expectations for the three- and five-year horizons increased by 0.1 percentage points to 3% and 2.7%, respectively.

The consumer price inflation (CPI) declined to 4.0 percent in May 2023, the lowest since March 2021 and slightly below market expectations of 4.1 percent, driven by a decline in energy prices. In addition, the core rate, which excludes volatile items such as food and energy, has slowed to 5.3 percent, the lowest since November 2021, supporting the argument for the Federal Reserve to consider pausing its current cycle of monetary tightening. Energy cost slumped 11.7 percent (vs -5.1 percent in April), while food inflation slowed to 6.7 percent (vs 7.7 percent in April). There were also smaller price increases for new vehicles (4.7 percent vs 5.4 percent), apparel (3.5 percent vs 3.6 percent), shelter (8.0 percent vs 8.1 percent), and transportation services (10.2 percent vs 11.0 percent). On a monthly basis, consumer prices edged up 0.1 percent in May after increasing 0.4 percent in April.

Producer prices for final demand decreased 0.3% month-over-month in May of 2023, following a 0.2% rise in April, and compared to market forecasts of a 0.1% drop. Goods prices went down 1.6%, the largest decrease since July 2022, mainly due to a 13.8% drop in gasoline prices and a 1.3% fall in food. Meanwhile, services cost edged 0.2% higher. Year-on-year, producer prices rose 1.1%, the least since December 2020.

The Fed left the target for the funds rate unchanged at 5%-5.25%, as expected, but signaled rates may go to 5.6% by year-end if the economy and inflation do not slow down more. It is the first pause in the tightening campaign following ten consecutive hikes that lifted borrowing costs to the highest level since September 2007. Policymakers said that holding the target range steady allows them to assess additional information and its implications for monetary policy, but noted they would be prepared to adjust it if risks emerge that could impede the attainment of their goals. The funds rate is now seen higher at 5.6% this year, compared to 5.1% projected in March. Upward revisions were also made for 2024 (4.6% vs 4.3%) and 2025 (3.4% vs 3.1%). The GDP is seen rising 1% this year, higher than the 0.4% seen in March, while growth for both 2024 (1.1% vs 1.2%) and 2025 (1.8% vs 1.9%) was revised lower. PCE inflation for this year is seen at 3.2%, below 3.3% in the March projection.

Retail sales unexpectedly rose 0.3% month-over-month in May of 2023, following a 0.4% increase in April, and beating forecasts of a 0.1% decline. The data signaled consumer spending remains resilient, despite higher inflation and interest rates. The biggest increases were seen in sales of building materials and garden equipment (2.2%) and motor vehicles and parts (1.4%). The so-called core retail sales which exclude automobiles, gasoline, building materials and food services, increased 0.2%, following a 0.6% gain in April.

The number of Americans filing for unemployment benefits remained at 262,000 on the week ending June 10th, sharply above market expectations of 249,000 to match the prior week’s upwardly revised value, the highest since October 2021.

The University of Michigan consumer sentiment increased to the highest in four months at 63.9 in June of 2023, from 59.2 in May, preliminary figures showed. Figures beat forecasts of 60, reflecting greater optimism as inflation eased and policymakers resolved the debt ceiling crisis. In June, improvements were seen in both current economic conditions (68 vs 64.9) and consumer expectations (61.3 vs 55.4). Also, year-ahead inflation expectations receded for the second consecutive month to 3.3%, the lowest since March 2021, from 4.2% in May. In contrast, long-run inflation expectations were little changed from May at 3%.

Have a great long holiday weekend,

Taylor Marr